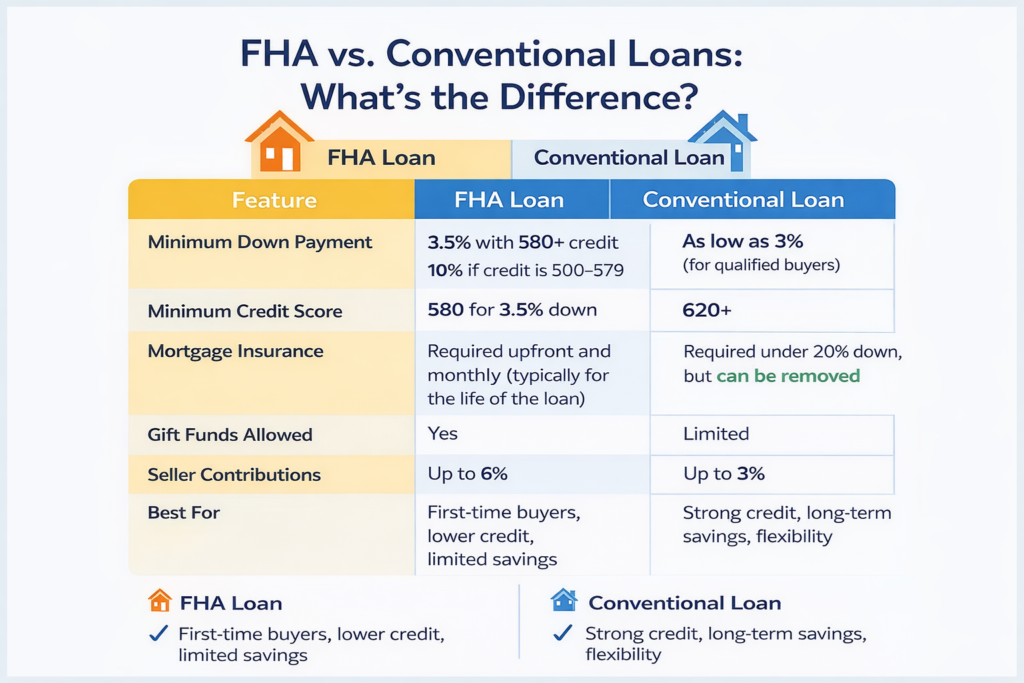

An FHA home loan is a government-insured mortgage designed to make homeownership more attainable. Backed by the Federal Housing Administration, FHA loans offer more flexible credit and down payment requirements than conventional loans, making them a popular choice for first-time buyers, those with limited savings, or borrowers working to rebuild their credit.

Yes! With an FHA 203(k) loan, you can roll both the home purchase and renovation costs into one mortgage.

Yes. FHA loans require both an upfront mortgage insurance premium (UFMIP) and ongoing monthly mortgage insurance (MIP).

Yes. FHA offers a streamline refinance option that allows you to reduce your interest rate with less documentation and no appraisal in many cases.

Mortgage insurance on FHA loans typically lasts for the life of the loan. However, if you put 10% or more down, MIP will automatically end after 11 years. Another way to remove it is by refinancing into a conventional loan once you have enough equity and qualify